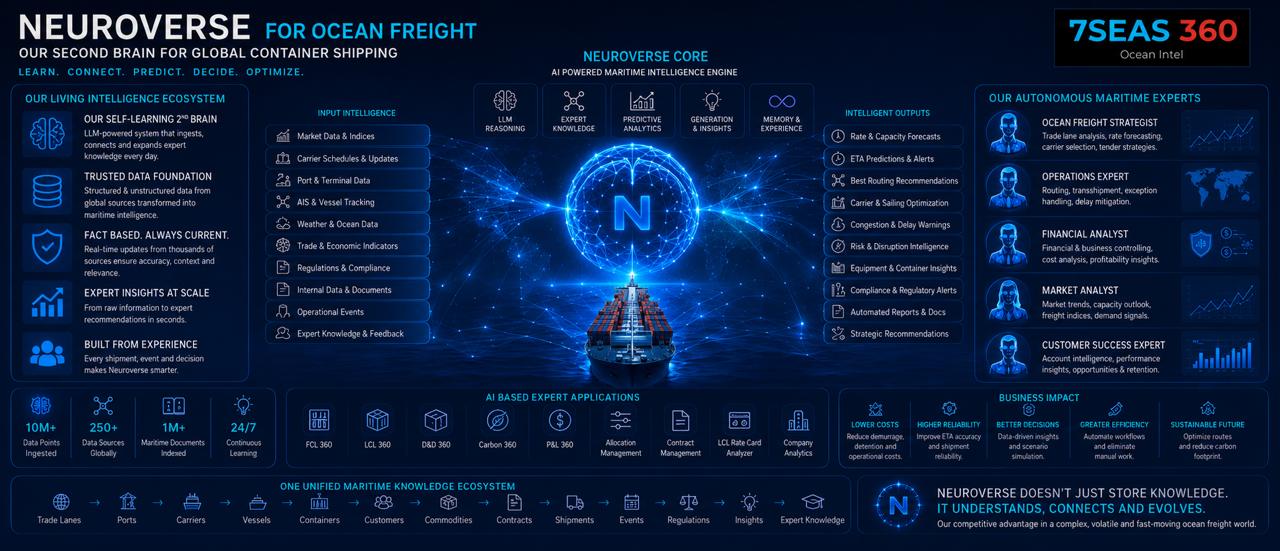

Maritime intelligence — curated daily from verified sources

Learn. Connect. Predict. Decide. Optimize.

Ocean freight has never been more complex. Shifting trade lanes, congested ports, volatile rates and disrupted routes mean the signals are everywhere, but the intelligence to act on them is scattered. At 7SEAS 360, we built something to change that.

Neuroverse is not a database that sits still. It is a self-learning ecosystem that ingests data from thousands of trusted global sources every day, including market indices, carrier schedules, port and terminal data, vessel tracking, weather, trade indicators and regulations, and transforms raw information into maritime intelligence in seconds. Every shipment, every event and every decision makes it smarter.

At its core, five capabilities work in concert: LLM reasoning, expert knowledge, predictive analytics, generation of insights and memory of experience. The result is a system that does not just store knowledge. It understands, connects and evolves.

On top of this core sit our autonomous maritime experts: an Ocean Freight Strategist, an Operations Expert, a Financial Analyst, a Market Analyst and a Customer Success Expert. Each one turns the intelligence of Neuroverse into forecasts, routing recommendations, risk alerts and strategic guidance you can use today.

And it powers the tools you already know: FCL 360, LCL 360, D&D 360, Carbon 360, P&L 360 and more. One unified knowledge ecosystem connecting trade lanes, ports, carriers, vessels, containers, contracts and beyond.

The impact is real: lower costs, higher reliability, better decisions, greater efficiency and a more sustainable future.

Neuroverse is our competitive advantage in a complex, volatile, fast-moving ocean freight world. Now it is yours too.

Industry insights, thought leadership, and deep dives — coming soon.

Two weeks into the renewed closure, the Strait of Hormuz is functioning as a war-risk exclusion zone for container shipping rather than a transit lane. Reported crossings collapsed to 10 on 12 July from a normal run rate near 88 a day, and the three carriers that dominate the Asia-Europe trade have now formally pulled their boxships out. Maersk is rerouting Gulf-bound cargo through Jebel Ali transhipment with Cape diversions on the mainline, CMA CGM has put all Asia-Europe services onto the Cape of Good Hope, and Hapag-Lloyd is doing the same with surcharges stacked on top of the Red Sea contingency adders already in force. The practical effect is a second simultaneous long-way-round detour on the world's busiest east-west corridor, and container diversions industry-wide are up roughly 360%.

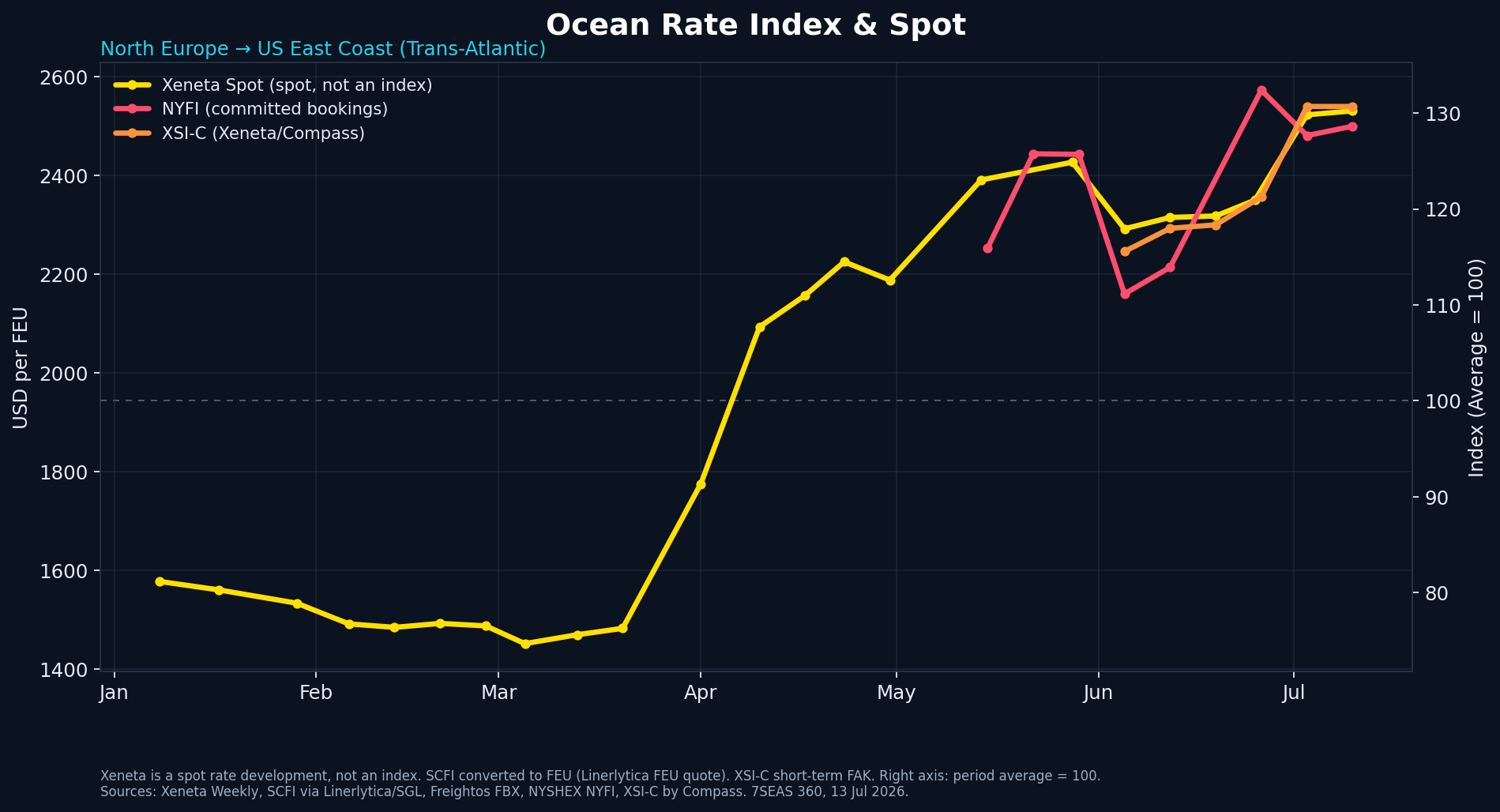

Rates are moving accordingly but unevenly. Asia-North Europe is around $5,500/FEU and Asia-Mediterranean has pushed past $7,000/FEU as the Med feels the Suez-plus-Hormuz squeeze most directly. Transpacific, structurally insulated from the strait, is still elevated at $7,069/FEU to the US West Coast and $8,808/FEU to the East Coast, with Shanghai-Los Angeles up about 253% on the late-February baseline; carriers layered $2,000-$3,000/FEU general increases on the Pacific from 15 July. The Gulf itself is the sharpest pain point: Jebel Ali, the region's principal transhipment hub, is congesting from diverted tonnage while Khalifa, Dammam and the Qatari, Bahraini and Kuwaiti ports sit largely cut off from mainline service. The geopolitical trigger remains live, with a 7,000-TEU vessel struck on 11 July and oil up about 10% and bunkers up 5% on the week, so the equipment repositioning and empty-container imbalances now building behind the Cape reroutes are likely to outlast any near-term de-escalation.

On 13 July the Hormuz crisis has hardened into an open dispute over whether the strait is even usable, layered on a wider kinetic exchange. Overnight into 12 July US Central Command launched a fresh round of strikes it framed as an effort to degrade Iran's capacity to attack civilian mariners and commercial ships transiting the strait. At least ten projectiles were reported on Qeshm Island, and explosions were reported across Bushehr, Bandar Abbas, Jask, Sirik, Konarak and Chabahar, with several military sites said to be hit. Striking port and coastal infrastructure directly, rather than inland targets, raises the operational risk to any commercial call in the lower Gulf. Iran responded on two tracks. The IRGC Navy declared the strait closed after saying it fired warning shots at a vessel on an unauthorised route, and Iran launched a drone attack on US rocket-launcher systems in Kuwait alongside further strikes touching Bahrain, Qatar and Oman. The result is a public contradiction: President Trump said the strikes had reopened the strait 'for business', while the IRGC and the Persian Gulf Shipping Association describe passage as impossible, and UKMTO and US Naval Forces Central Command maintain that the southern lane remains an international waterway carrying two-way traffic. For container shipping the argument is academic against the traffic data. Windward recorded about 21 commercial transits on 11 July, split roughly 12 outbound and 9 inbound, against a pre-crisis baseline near 88 a day and an ordinary peacetime flow far higher still. The Combined Maritime Forces' Joint Maritime Information Center held the strait threat level at SEVERE on 12 July. The big four box lines have not moved off suspension: Maersk continues to route Gulf-bound cargo via Jebel Ali transhipment with Cape diversions for Asia-Europe, CMA CGM and Hapag-Lloyd keep Asia-Europe on the Cape of Good Hope, and MSC limits Gulf calls, with Cape routing still adding 10 to 14 days per voyage. On price the escalation continues to stack on an already firm peak season. Asia-North Europe has risen to about $5,400 per FEU and Asia-Mediterranean has passed $7,000, both building on gains since mid-May, while the transpacific holds near its recent highs above the $7,000s per FEU. Carriers are pressing the increases through: HMM has set a peak-season surcharge of $3,000 per 40ft container effective 15 July, and emergency conflict surcharges of $2,000 to $4,000 per box are being applied on affected trades on top of standing Gulf surcharges, with war-risk cover still running at a multiple of normal. Practical takeaway for shippers: discount the open-versus-closed messaging and plan on the strait being unusable for scheduled container services, keep Asia-Europe on Cape transit times with the extra 10 to 14 days through at least the rest of the quarter, lock transpacific and Asia-Europe space and budget ahead of the 15 July surcharge round, and watch three tracks, whether the strikes on Iranian ports draw a wider Gulf response, the security of Kuwait, Bahrain, Qatar and Oman after the retaliation, and any move toward a renewed ceasefire, before assuming a return to the strait.

On 10 July the Hormuz picture has moved from a tested ceasefire to no ceasefire. President Trump said at the NATO summit that he now considers the US-Iran ceasefire 'over' and that further negotiations would be a 'waste of time', after Iranian attacks on commercial vessels in the strait and mutual accusations of violating the interim deal. That statement removes the diplomatic floor that had underpinned any near-term reopening. The kinetic exchange has widened rather than cooled: the US military said its latest round of airstrikes hit around 90 targets across Iran, up from the 80-plus reported on 8 July, and Iran retaliated with a wave of strikes on three Gulf states that set off alerts in Qatar, Bahrain and Kuwait. The Gulf Cooperation Council condemned the earlier Iranian attacks on the Saudi commercial vessel Wadiyan and the Qatari LNG carrier Al Rekayyat as they transited the strait. For container shipping the direct hits remained tankers, but the operating consequence is that the strait is now treated as closed. Transits are running near 34 a day against a pre-crisis baseline of about 88, and the big four box lines have hardened from diversion to suspension. Maersk has stopped new Hormuz transits and is routing Gulf-bound cargo via Jebel Ali transhipment while diverting Asia-Europe around the Cape of Good Hope, CMA CGM has activated Cape routing for all Asia-Europe services, Hapag-Lloyd has suspended Hormuz transits and reroutes via the Cape, and MSC is running Asia-Europe via the Cape with Gulf calls limited to escorted convoys. Cape routing continues to add 10 to 14 days per voyage and a double-digit cost premium. On price, the escalation stacks on top of an already firm early peak season: Asia-Mediterranean rose another 11% week on week for the week ending 8 July, transpacific spot pushed past $7,900 per FEU, and the July GRIs and PSS have held, adding more than $3,000 per FEU on the transpacific since late May, with carriers layering Gulf and India-Pakistan surcharges of about $1,000 per container on top. War-risk insurance is running near eight times normal. The commercial dispute that dominated late June, Iran's plan to levy service fees on transiting vessels once the free-passage window closes in mid-August, is now secondary to live hostilities. Practical takeaway for shippers: treat the strait as closed for container routing, plan Asia-Europe on Cape transit times with the extra 10 to 14 days for the rest of the quarter, lock transpacific and Asia-Europe space early given firm peak-season rates, budget for sustained war-risk and surcharge exposure, and watch three tracks, whether any new ceasefire attempt emerges after this exchange, the security of the wider Gulf after the strikes on three states, and mine-clearance and safety certification, before assuming any return to the strait.

On 8 July the Hormuz picture has re-escalated sharply. Iran's Revolutionary Guard fired missiles at three commercial vessels in roughly 24 hours, two on the night of 6 July and a third on the morning of 7 July, striking a Qatari LNG carrier reported as the Al Rekayyat and a Saudi-flagged crude tanker among them; both ships were significantly damaged, an engine-room fire was reported, and all crew were confirmed safe. Al Jazeera and Reuters describe it as the heaviest day of attacks on shipping since the US-Iran peace deal, and it directly tests the negotiations meant to reopen the strait. The United States responded in kind: CENTCOM said early on 8 July that it had completed a round of strikes on more than 80 targets, air-defence systems, coastal radar sites and dozens of IRGC small boats, describing the operation as an effort to degrade Iran's ability to disrupt international maritime trade. The vessels hit this time were tankers rather than container ships, so the direct damage sits outside the box-shipping scope, but the consequence for container shipping is real and negative. With live missile exchanges back in and around the strait, Maersk, MSC, CMA CGM and Hapag-Lloyd remain committed to the Cape of Good Hope and have reissued safety guidance prioritising crews, and Hormuz throughput holds near 25 transits a day against a pre-war baseline near 110. Any hope of a near-term container return to the strait has slipped further out. On price, the most recent Freightos print, for the week ending 2 July, put Asia-North Europe at $2,707 per FEU, up 11% on the week, and Asia-Mediterranean at $3,850 per FEU, up 15%, and the fresh escalation adds upside pressure rather than relief; Brent crude moved toward $73 a barrel on the attacks, lifting bunker and war-risk cost exposure for any Gulf-linked service. The commercial dispute is now entangled with live hostilities: Doha talks continue, but Iran keeps signalling it will charge service fees on transiting vessels once the 60-day free-passage window closes around 17 August, framing them as service charges rather than tolls, and the US is resisting that. Practical takeaway for shippers: treat the strait as unsafe for container routing and do not plan direct Gulf transits on it, hold Asia-Europe on Cape transit times with the extra 10 to 14 days built in for the rest of 2026, lock transpacific and Asia-Europe space early given firm peak-season rates, budget for continued surcharge and war-risk exposure, and watch three tracks now, the durability of the ceasefire after this exchange, mine-clearance and safety certification, and the toll-versus-fee outcome in Doha, before assuming any normal return to the strait.

On 6 July the Hormuz recovery has stalled and partly reversed. The IMO-Oman corridor that finally appeared on the chart in late June is not holding: between 2 and 3 July at least eight commercial vessels that tried the toll-free route were forced to turn back under IRGC threat, with Windward tracing movement patterns consistent with the turn-back orders, and the IRGC restating that the only authorised transit routes are the ones Iran designates and that ships must maintain VHF contact with its navy while crossing. Traffic has slipped in step, with roughly 25 to 35 transits a day recorded on 2 to 4 July against a pre-war baseline near 110, well down from the 70-crossing single-day peak on 25 June; Lloyd's List notes vessels keep moving in small numbers but the IMO evacuation scheme stays suspended after the late-June strike on the Ever Lovely. For container shipping the posture has hardened rather than eased. Maersk, MSC, CMA CGM and Hapag-Lloyd have now confirmed their Cape of Good Hope contingency will remain fully funded and operational for the remainder of 2026, with schedules and service contracts rebuilt around the longer routing, so the extra roughly 3,500 nautical miles and 10 to 14 days on each Asia-Europe voyage are baked into the network and Gulf calls stay limited to escorted convoys. That entrenched capacity drain, on top of peak-season demand, keeps rates rising: Freightos puts Asia-North Europe at $2,707 per FEU, up 11% on the week, and Asia-Mediterranean at $3,850 per FEU, up 15%, as carriers implement FAK increases and peak-season surcharges, while transpacific to the US West Coast is running about 40% above pre-war levels and Asia-North Europe about 20% above, and Gulf-linked emergency surcharges reach $3,000 per FEU. The newest layer is commercial rather than military. The Islamabad Memorandum guarantees free passage for 60 days, but Iran is now signalling it will levy service and insurance fees on transiting vessels once that window closes, framing them as charges for services rather than tolls, and the US is resisting that in the Doha talks. Even if a channel is eventually certified clear, shippers may face a new per-transit cost in the Gulf. Practical takeaway for shippers: treat the IMO corridor as unreliable and do not plan direct Gulf container routing on it, keep Asia-Europe on Cape transit times with the extra 10 to 14 days built in for the rest of 2026, lock transpacific and Asia-Europe space early given firm peak-season rates and thin blank-sailing cushion, budget for continued surcharge exposure, and watch two tracks now, mine-clearance certification and the toll-versus-fee outcome in Doha, before assuming any normal return to the strait.

On 1 July the Hormuz picture takes a meaningful step toward normalization without actually clearing. The development that was missing on 29 June, a single verified safe channel, now exists on paper: on 27 June the US Navy-led Joint Maritime Information Center widened its recommended route near Oman, and Oman opened a temporary maritime corridor coordinated with the IMO, with vessels asked to follow the published coordinates and coordinate their passage. Traffic has kept recovering behind that, with Kpler recording 70 crossings on 25 June, the highest single-day count since the 1 March closure, though still under 60% of the roughly 120 transits a day seen before the war. For container shipping the practical posture has not yet changed. The nine largest carriers keep Asia-Europe sailings on Cape of Good Hope routing with their crisis surcharges intact, adding about 3,500 nautical miles and 10 to 14 days per voyage and holding any Gulf calls to escorted convoys, so roughly 10% of global container capacity stays tied up in the longer routing. The reason box lines are slower to return than tankers is the mine question: reports that Iran lost track of mines it planted mean the strait cannot be certified clear, and the IRGC has publicly warned vessels off the new route, so carriers read the corridor as a naval and tanker channel first, not yet a dependable lane for scheduled liner services. That capacity drain keeps rates firm. Drewry's composite World Container Index stands at $4,166 per 40ft as of 25 June, a 22-month high, led by the Pacific, where Shanghai to Los Angeles rose 12% to $5,750 per FEU and Shanghai to New York rose 6% to $7,149 per FEU as importers frontload ahead of the 24 July expiry of the Section 122 tariff surcharge; July peak-season surcharges and general rate increases are filed across both basins. Underneath it all a backlog of about 2,300 vessels, including roughly 1,566 cargo ships, is still queued in the Gulf and Gulf of Oman, which will keep container equipment and box positions dislocated and schedules unreliable even as the corridor slowly draws the queue down. Practical takeaway for shippers: treat the IMO corridor as real progress but not a green light for direct Gulf container routing, keep Asia-Europe planned on Cape transit times with the extra 10 to 14 days built in, lock transpacific space early given the frontloading and thin blank-sailing cushion, budget for a firmer July across both basins, and watch mine-clearance certification and IRGC signals before assuming liner services return to the strait.

On 29 June the Hormuz picture is genuinely two-sided. On the traffic side it looks like a recovery: Lloyd's List Intelligence recorded 49 transits on 24 June and 43 on 25 June against a pre-crisis baseline near 93, and about 125 vessels in the week after the ceasefire, the highest weekly count since the war started in late February. On the risk side the recovery is anything but settled. The Singapore-flagged Evergreen container ship Ever Lovely was struck by a projectile roughly 7.5 nautical miles off the Omani coast on 25 June as it left the strait, damaging the bridge superstructure; all 21 crew were unharmed and US officials attributed the strike to the IRGC, after which the IMO paused its evacuation scheme for ships still trapped in the Gulf. For container shipping the practical posture has not changed: Maersk, MSC, CMA CGM and Hapag-Lloyd are keeping Asia-Europe sailings on Cape of Good Hope routing, which adds about 3,500 to 4,000 nautical miles and 10 to 14 days per voyage and soaks up vessel capacity, with MSC charging $1,200 per TEU and Gulf calls limited to escorted convoys. That capacity drain keeps rates firm. Drewry's composite World Container Index rose 5% to $4,166 per 40ft on 25 June, led again by the Pacific, where Shanghai to Los Angeles jumped 12% to $5,750 per FEU and Shanghai to New York rose 6% to $7,149 per FEU as importers frontload ahead of tariff changes; Asia-Europe held firmer-to-flat with Shanghai to Rotterdam up 1% to $4,392 per FEU. July peak-season surcharges and general rate increases are filed across both basins. The one clear de-escalation signal is diplomatic: on 28 June the US and Iran halted attacks and agreed to resume Hormuz talks in Doha, and war-risk premiums have eased to roughly eight times pre-crisis levels from a peak near 4,000 times. Practical takeaway for shippers: treat the traffic rebound as real but reversible, keep Asia-Europe planned on Cape transit times with the extra 10 to 14 days built in, lock transpacific space early given the frontloading and a thin blank-sailing cushion, budget for a firmer July across both basins, and watch the Doha track and a single verified safe channel before assuming any return to direct Gulf routing.

On 26 June the Hormuz story is less about the strait itself moving and more about where the rate pressure is now landing. For container shipping the Asia-Europe picture is unchanged: the four mega-carriers, Maersk, MSC, CMA CGM and Hapag-Lloyd, are keeping their Gulf restrictions and Cape of Good Hope routing in place despite the diplomatic push to reopen, and the Cape detour continues to add 10 to 14 days per voyage, soaking up vessel capacity and keeping supply tight. What has shifted this week is the transpacific. Drewry's composite World Container Index rose 5% to $4,166 per 40ft on 25 June, but the move was led by the Pacific rather than Europe: Shanghai to Los Angeles jumped 12% to $5,750 per FEU and Shanghai to New York rose 6% to $7,149 per FEU, with importers frontloading ahead of expected tariff changes and only four blank sailings announced for the coming week. Asia-Europe lanes remain elevated in parallel, with North Europe quotes above $2,700 per FEU and Mediterranean rates around $3,850 to $4,000 per FEU. Underneath the rates, the geopolitical base is still unsettled. A 17 June memorandum of understanding promised 60 days of no-charge transit through Hormuz, but Iran re-declared the strait closed on 20 June after strikes on Lebanon, and reported traffic has swung between roughly 5 and 35 vessels a day against a pre-crisis baseline near 93. US and Iranian negotiators established a communication line in Geneva on 21 June to deconflict and assure safe passage during the window, yet many vessels are still dimming AIS and hugging the Omani shoreline, so the channel stays opaque for container lines weighing a return. Practical takeaway for shippers: budget for a firmer July across both basins, lock transpacific space early given the frontloading and thin blank-sailing cushion, keep Asia-Europe on Cape transit times with the extra 10 to 14 days built in, and treat the 60-day Hormuz window as a fragile arrangement rather than a reopening until a single verified channel and stable insurance terms hold.

The Hormuz picture on 24 June is one of structure hardening around the disruption rather than easing out of it. Instead of a clean reopening, a dual-transit regime is taking shape: an Iranian-controlled northern route and a US-backed southern corridor routed through Omani territorial waters, leaving masters to pick between two channels that neither side has fully verified as safe. For container carriers that is not a signal to come back. The mine problem underneath the diplomacy is the harder constraint. Reporting indicates Iran has lost track of mines it laid and therefore cannot fully reopen the waterway, while clearance using underwater drones is still assessed at 40 to 50 days. On the water, transits rebounded over 19 to 21 June, with Kpler counting roughly 71 crossings and a weekend peak near 35, but Iran declared the strait closed again on 20 June and the flow that does move is dominated by escorted tankers, not boxships. Commercial container traffic sits at about 5 to 10% of pre-February levels. The carrier response is unchanged and firm: Maersk, MSC, CMA CGM and Hapag-Lloyd keep suspending or tightly limiting new Hormuz bookings and continue routing Asia-Europe around the Cape of Good Hope, with Gulf-linked capacity running near 40,000 TEU a week against roughly 100,000 before the crisis and a partial recovery to 50,000 to 60,000 TEU only expected later in July. Rates and surcharges are moving up in step. Shanghai-Rotterdam reached about $4,340 per FEU, up around 15%, and Shanghai-Genoa about $5,760 per FEU, up around 12%, with North Europe quotes frequently above $5,000. Maersk has now fixed concrete July peak-season surcharges: $750 per TEU on Far East to North Europe and Mediterranean from 7 July, $1,800 per TEU to Southern Africa and Indian Ocean Islands and $1,000 per 40ft to the Middle East from 1 July. Practical takeaway for shippers: treat the dual-corridor arrangement as fragile, book and budget July Asia-Europe space now with the new surcharges priced in, and keep an extra 7 to 14 days of transit buffer until a single verified channel, mine clearance and stable insurance terms are in place.

The Hormuz reopening that looked underway last week wobbled on 20 June, when Iran declared the strait closed again over alleged Israeli ceasefire violations and Washington's failure to implement the first clause of the 17 June Islamabad memorandum. The IRGC navy renewed mine and targeting warnings to passing ships. US Central Command countered that the waterway never closed and recorded 55 merchant transits on 20 June, a post-war high, but those crossings are dominated by escorted tankers, not container ships. For box carriers the contradiction is the story: until safety is verified and consistent, lines will not unwind Cape of Good Hope routings they spent four months building. Maersk and MSC continue to send Asia-Europe services around southern Africa and put full schedule restoration at six to eight weeks after a durable reopening, since contracts, vessel positioning and fuel procurement for the rest of 2026 already assume the Cape. On the water, commercial transits sit at roughly 5 to 10% of pre-February levels, fewer than ten vessels a day versus over a hundred before, and the central deep-water channel stays shut pending clearance of around 80 mines, an estimated 40 to 50 days of work, while war-risk surcharges remain elevated. The rate picture moves the opposite way from the diplomacy. Xeneta assesses Asia-North Europe near $2,880 per FEU, about 30% above pre-crisis, and carriers are rolling cargo, cutting allocations and layering mid-June GRI and PSS steps of $1,000 to $2,000 per FEU with further July increases of up to $2,000 per FEU. An early peak season, driven by frontloading ahead of bunker adjustments, tariffs and the July hikes, is tightening origin space and worsening equipment imbalances exactly as the Hormuz queue holds boxes and ships out of position. Practical takeaway for shippers: treat the reopening as reversible, lock July space and rates early, and keep an extra 7 to 14 days of buffer in Asia-Europe plans until transits, mine clearance and insurance terms hold steady.

After nearly four months of closure, the Strait of Hormuz is moving toward reopening under a US-Iran agreement formally signed today. The 14-point Islamabad Memorandum of Understanding triggers a 60-day negotiation period and commits Iran to allow toll-free transit for at least 60 days. For container shipping the relief is real but slow. Roughly 100 boxships, about 10% of the global fleet, are among the 750-odd vessels ensnared in the Hormuz region, and executives warn it will take weeks to clear the queue as ships converge on UAE and Saudi ports. The bigger drag on the Asia-Europe trade is structural: the top four lines, Maersk, MSC, CMA CGM and Hapag-Lloyd, suspended Hormuz transit in early March, and most have rebuilt 2026 schedules, contracts, vessel positioning and fuel procurement around the Cape of Good Hope, the routing already forced by the Houthi campaign. Unwinding those arrangements is not a switch lines will flip on a memorandum alone. Two risks keep carriers cautious: residual underwater mines and war-risk insurance premiums that remain high despite the diplomatic breakthrough, prompting the industry to demand operational clarity before normal calls resume. On rates, the spike has largely unwound, with Asia-North Europe spot near $2,850/FEU and drifting back toward pre-war levels, though equipment imbalances, blank-sailing adjustments and a peak-season pull-forward ahead of the 1 July bunker adjustment are keeping origin bookings tight. Shippers should still buffer an extra 7 to 14 days into May and June plans until the backlog drains and security guarantees firm up.

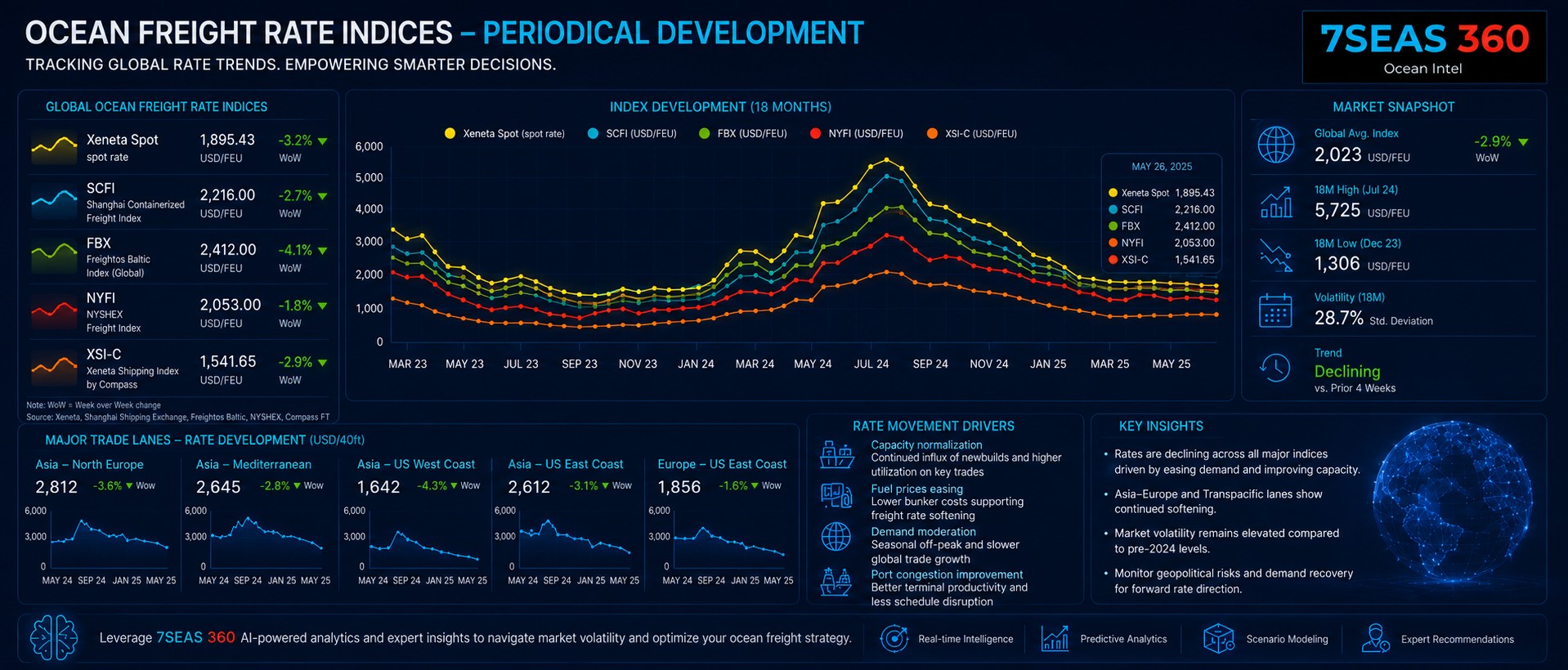

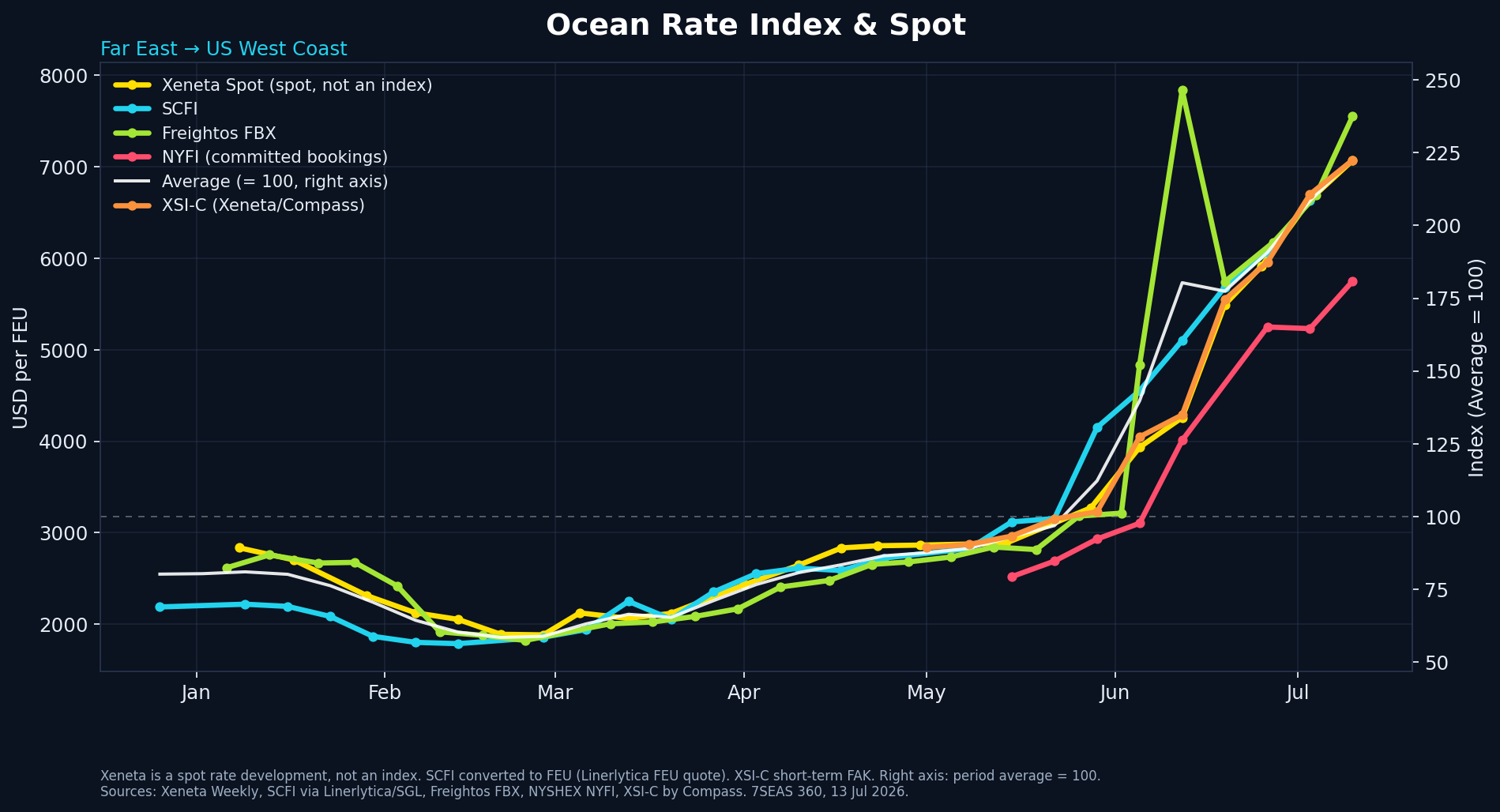

Almost four months after the Strait of Hormuz effectively closed to commercial shipping on 28 February, the waterway remains a ghost route and the container market is now driven more by the secondary effects of the conflict than by the strait itself. With most lines avoiding the Gulf and rerouting Asia-Europe and Asia-US East Coast services around the Cape of Good Hope, voyages run 10 to 14 days longer, an estimated 5 to 7% of global fleet capacity is locked up in steaming distance, and box availability has tightened. Spot rates have surged across every east-west trade: Xeneta puts Far East-US West Coast at $3,933/FEU, up 109% since the crisis began, while Asia-Europe lanes are up 51 to 65% and the broader market index has risen sharply on early peak-season frontloading. Congestion at the Singapore and Port Klang transshipment hubs, where carriers are rebuilding networks around the blockade, is compounding delays, and bunker costs roughly 70% higher are flowing through to surcharges. Around 138 container ships with close to 470,000 TEU stay stranded inside the Persian Gulf. On the geopolitical side, a fragile US-Iran ceasefire faltered in early June, the US naval blockade of Iranian ports has expanded into the Indian Ocean with tanker boardings, and reopening talks continue without shipowners showing willingness to return. For shippers, the practical message holds: plan for Cape routings, longer transit times, elevated rates and fuel surcharges through the summer, and book early.

The Strait of Hormuz had its most important day since the closure began, but it happened in a conference room rather than on the water. On 14 June the United States and Iran announced a framework to extend the ceasefire and reopen the Strait, with a formal accord set for signing on 19 June in Switzerland. For container shipping the signal matters, yet the working reality for the week ahead is unchanged. Daily transits were still a trickle in early June, roughly two on 7 June against a normal flow near 100 ships, and the major box carriers, Maersk, MSC, CMA CGM and Hapag-Lloyd, are keeping Hormuz transits suspended until the ceasefire proves it can hold. Insurers are taking the same cautious line: war risk premiums and Gulf surcharges price off verifiable stability rather than political statements, so cover stays near crisis levels and the Arabian Gulf remains a listed conflict zone for now. That keeps the Cape of Good Hope as the default routing for Asia-Europe strings, our top-priority corridor, adding 10-14 days per round trip and holding effective capacity tight. The twist this week is on the demand side. An early peak season is lifting spot rates on both the Asia-Europe and transpacific lanes just as the Cape detour absorbs capacity, so the two forces now stack: shippers face firm and rising rates even as the headlines turn toward peace. The honest read for planners is that a signed accord on 19 June starts a clock, it does not flip a switch. Carriers will want escorted proof of safe passage, restored insurance terms and a stable security picture before they unwind Cape rotations, and the equipment stranded inside the Gulf will take weeks to recirculate once they do. For the coming days the assumption remains Cape routing, elevated rates and a watchful eye on whether the 19 June signing turns an announcement into open water.

More than three months into the closure, the Strait of Hormuz has shifted from an acute shock to a structural fact that container shipping is now planning around rather than waiting out. On the priority Asia-Europe corridor, carriers have stopped treating the Cape of Good Hope as an emergency detour and have made it the default, adding 10-14 days and an estimated 5-7% of global effective capacity to absorb the longer rotations. That capacity drain, more than any surge in demand, is what keeps Asia-North Europe spot rates near $2,850/FEU and roughly a fifth above pre-conflict levels. The transpacific lane, second in our hierarchy, is carrying the spillover: Shanghai spot rates to Los Angeles and New York are up between 59% and 129% since late February as vessels and equipment are pulled toward the rerouted networks, even though West Coast service delays remain modest. The Middle East lane itself stays largely cut off, with only a trickle of transits versus the usual ~100 ships a day. The subtler risk sits in equipment: empty and reefer boxes are stranded in Gulf ports and cannot cycle back to Asian load centres, so even as the share of the global boxship fleet held inside the Gulf eases from its 1.4% peak toward 1.0%, the imbalance threatens box availability on lanes far from the conflict. Maersk, which has not moved a ship out of the Gulf since mid-May and is trucking cargo around the Strait, illustrates the cost: carriers are paying for longer voyages, higher fuel and idle equipment with no clear reopening date. For shippers, the planning assumption for the coming weeks is continuity of disruption, not relief.

The Strait of Hormuz reaches roughly its 102nd day of effective closure since the February 28 outbreak of conflict, and the container market is now absorbing a double shock: an unresolved chokepoint and the start of peak season. IMF PortWatch data shows commercial transit stuck at about 11% of pre-crisis volume — roughly 10 vessels per day against a normal ~95. Around 100 containerships remain trapped inside the Arabian Gulf, and Maersk reports it has not had a ship leave the Gulf since mid-May, with six of its vessels still stranded inside. All major carriers — Maersk, MSC, CMA CGM, Hapag-Lloyd, COSCO and Evergreen — maintain suspended Gulf bookings and force-majeure postures, with COSCO, CMA CGM and Hapag-Lloyd halting new bookings across a wide range of Middle East Gulf destinations.

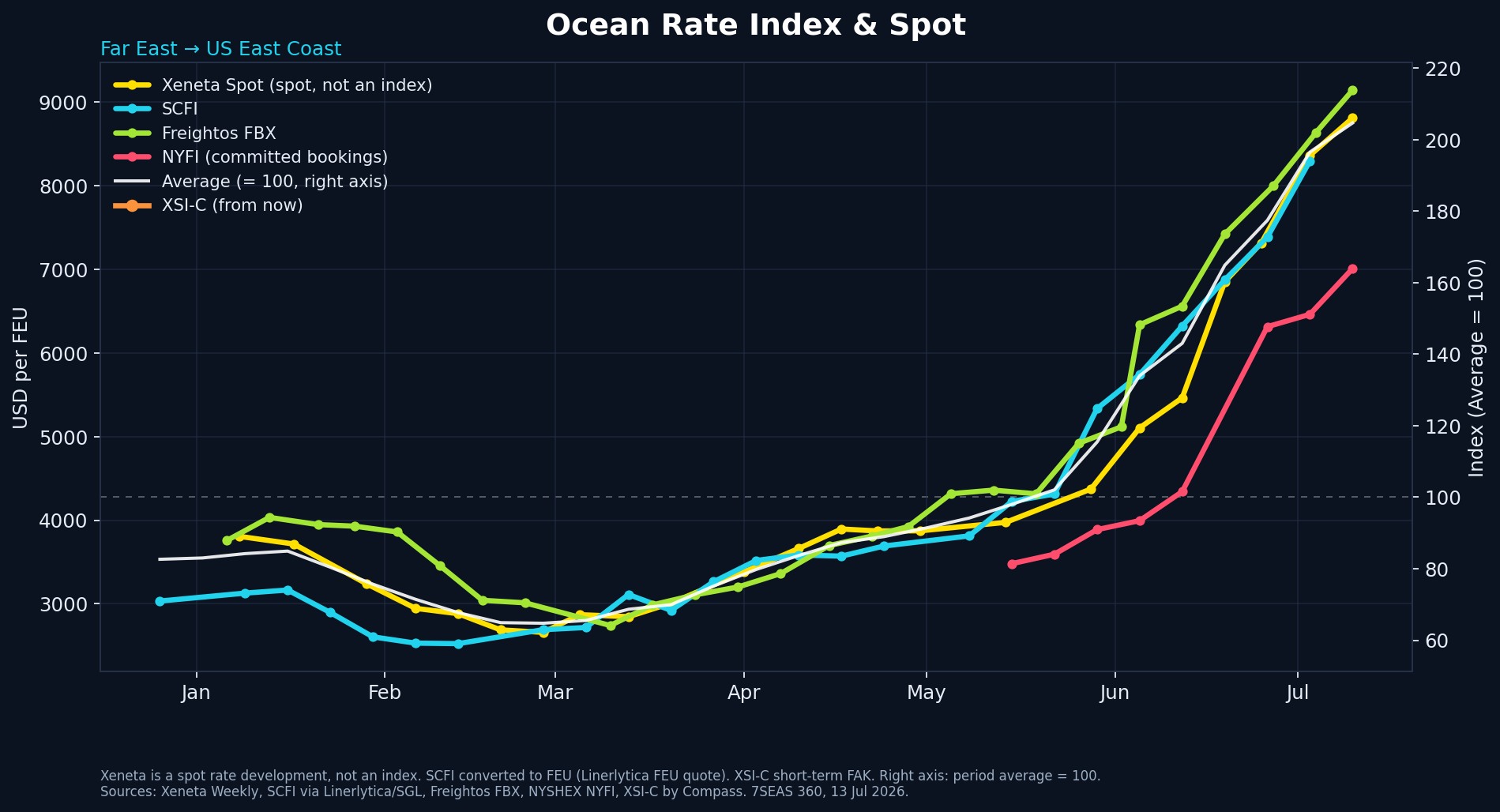

Rerouting via the Cape of Good Hope is now structural: MSC moves all Asia-Europe strings via the Cape at a $1.2k/TEU surcharge, while Maersk runs Jebel Ali transhipment plus Cape diversions at roughly $1.0k/TEU. The capacity drain, compounded by June 1 GRIs and peak-season surcharges, is driving rates sharply higher: Far East-USWC sits at $3,933/FEU (+109% versus pre-conflict), Far East-USEC at $5,103/FEU, Far East-North Europe at $3,649/FEU (+27% in a single week) and Far East-Mediterranean at $5,041/FEU.

On the geopolitical side, Washington is quietly assisting willing shippers through a low-profile version of 'Project Freedom' — CENTCOM says it coordinates with rather than formally escorts commercial vessels, which transit with transponders off, hugging the Omani coast to avoid Iranian mines. Between 30 and 70 ships are reported to have crossed since early May, but war-risk premiums remain roughly 4,000 times pre-crisis levels, and the DFC's $40bn government reinsurance backstop has still written zero business and covered zero transits. Equipment imbalances continue to deepen as empty-container repositioning to Gulf origins stays impossible, and recovery timelines remain measured in weeks to months even after any resolution.

The Strait of Hormuz reaches roughly its 100th day of effective closure since the February 28 outbreak of conflict, and the container market is now absorbing a double shock: an unresolved chokepoint and the start of peak season. IMF PortWatch data shows commercial transit stuck at about 11% of pre-crisis volume — roughly 10 vessels per day against a normal ~95. Around 100 containerships remain trapped inside the Arabian Gulf, and Maersk reports it has not had a ship leave the Gulf since mid-May, with six of its vessels still stranded inside. All major carriers — Maersk, MSC, CMA CGM, Hapag-Lloyd, COSCO and Evergreen — maintain suspended Gulf bookings and force-majeure postures, with COSCO, CMA CGM and Hapag-Lloyd halting new bookings across a wide range of Middle East Gulf destinations.

Rerouting via the Cape of Good Hope is now structural: MSC moves all Asia-Europe strings via the Cape at a $1.2k/TEU surcharge, while Maersk runs Jebel Ali transhipment plus Cape diversions at roughly $1.0k/TEU. The capacity drain, compounded by June 1 GRIs and peak-season surcharges, is driving rates sharply higher: Far East-USWC sits at $3,933/FEU (+109% versus pre-conflict), Far East-USEC at $5,103/FEU, Far East-North Europe at $3,649/FEU (+27% in a single week) and Far East-Mediterranean at $5,041/FEU.

On the geopolitical side, Washington is quietly assisting willing shippers through a low-profile version of 'Project Freedom' — CENTCOM says it coordinates with rather than formally escorts commercial vessels, which transit with transponders off, hugging the Omani coast to avoid Iranian mines. Between 30 and 70 ships are reported to have crossed since early May, but war-risk premiums remain roughly 4,000 times pre-crisis levels, and the DFC's $40bn government reinsurance backstop has still written zero business and covered zero transits. Equipment imbalances continue to deepen as empty-container repositioning to Gulf origins stays impossible, and recovery timelines remain measured in weeks to months even after any resolution.

Ninety-six days after the Strait of Hormuz effectively closed on 28 February, it remains shut to container shipping. Xeneta describes the strait as still closed to boxships, with roughly 100 containerships trapped inside the Arabian Gulf — Hapag-Lloyd alone reports four vessels stuck, one of them in transit for four weeks. Daily transits have collapsed to around 10 ships versus about 95 in normal times, and the few crossings that do happen are mostly US-escorted, high-risk runs that do not signal a return to normal traffic.

The freight impact has settled into a sustained plateau rather than a fresh spike: Xeneta's June data shows spot rates up 75% from China to the US East Coast, 51% to North Europe, 45% to the Mediterranean and 57% on the transatlantic versus pre-conflict levels. War-risk insurance — the single biggest deterrent to crossing — sits near 4% of a ship's hull value for seven days of cover, roughly 4,000 times pre-crisis pricing.

Carriers continue to route Asia-Europe and Gulf cargo around the Cape of Good Hope, adding 3,500-4,000 nm and 10-14 days per voyage and pulling 10-20% more tonnage into the same loops; Gulf-destined boxes are transshipping via Salalah and Khor Fakkan onto feeder and landbridge networks. Crucially, the market is not behaving like a clean supply shock: a structural capacity glut is offsetting much of the Hormuz disruption, and Linerlytica reports that carriers keep announcing FAK increases only to undercut them when utilisation fails to hold.

On the diplomatic track, a US-Iran framework for a 60-day ceasefire extension and a phased reopening has been floated, with Iran expected to clear the mines it laid — but Tehran reported no negotiating progress as of 3 June, reports suggest Iran has lost track of some of its own mines, and a 15-nation mine-clearing coalition led by the Royal Navy and France is only now taking shape. Recovery remains a matter of weeks to months even once a deal lands, and equipment imbalances continue to deepen as empty repositioning to Gulf origins stays impossible.

More than three months after traffic through the Strait of Hormuz seized up on 28 February, the chokepoint remains effectively closed to container shipping — transit is running at only about 5% of the pre-war norm. The end of the US naval blockade of Iranian ports on 29 May has not restored confidence: most carriers are unwilling to send boxships through the 21-mile channel until a durable peace deal explicitly guarantees safe passage.

Maersk has not had a vessel leave the Gulf since mid-May and has six ships stranded inside, while MSC continues to route every Asia–Europe service around the Cape of Good Hope. Xeneta estimates the conflict has displaced roughly 250,000 TEU of weekly capacity, with carriers leaning on landbridge and transhipment workarounds via Jebel Ali, Khor Fakkan, Sohar and Jeddah rather than risking direct transits.

The cost shows up in rates and reliability: Asia–North Europe spot pricing sits around $2,880/FEU, up about 30% on pre-conflict levels, and China–Jebel Ali rates have surged more than 270% since end-February. Cape reroutes add about two weeks per leg and keep major Indian and Gulf-feeder ports congested.

On the geopolitical side, a conditional ceasefire mediated by Pakistan remains fragile; Iran is policing the strait under new IRGC procedures and demanding tolls above $1 million per ship, a practice maritime authorities reject under international law. For shippers, the practical takeaway is unchanged: plan for Cape transit times, persistent surcharges, and severe equipment shortages on Gulf-origin lanes for weeks to come, even if the ceasefire holds.

Six weeks into the blockade, the Strait of Hormuz remains effectively closed to mainstream container traffic. Vessel transponder data shows Hormuz running at roughly 5% of its pre-war average, and commercial operators emptied the waterway again this week after a second round of US strikes against Iranian military targets. Iran's Islamic Revolutionary Guard Corps has formalised control via a new 'Persian Gulf Strait Authority', requiring full coordination and clearance from Iranian forces for any passage.

The IRGC reported coordinating 26 transits in 24 hours on May 20, but talks with Washington over a wider reopening remain stalled and the US-led 'Project Freedom' escort initiative has so far moved only a handful of ships, including the Maersk-operated Alliance Fairfax in early May.

For container shipping, the structural impact is now visible in spot rates: Asia-N. Europe has risen $300/FEU since end-April to $2,900/FEU, matching the late-March wartime high, while Asia-Mediterranean spiked 20% in one week to nearly $4,400/FEU, a fresh wartime peak. Carriers are layering on GRIs and PSSs of $600 to over $1,000/FEU through mid-June, citing Red Sea diversions, longer transit times via the Cape of Good Hope, and frontloading ahead of new July BAFs.

Maersk, MSC, CMA CGM, Hapag-Lloyd and COSCO all keep Gulf bookings suspended; CMA CGM still has 14 vessels stranded inside the Gulf, and major lines are shifting tonnage toward India as a transhipment workaround. Equipment imbalances continue to deepen — empty repositioning to Gulf origins remains effectively impossible, and shippers are now planning around sustained alternative routing through the second half of 2026.

Five weeks after the U.S.–Iran ceasefire took effect, the Strait of Hormuz has not reopened in any meaningful commercial sense. According to Xeneta and Safety4Sea, the corridor remains effectively closed to standard container shipping, with vessel movement permitted only through IRGC-managed routing and selective clearance codes. Kpler's two-month assessment confirms that of the 53 container vessels trapped inside the Persian Gulf when transits became untenable, only around nine have successfully exited; two MSC boxships were seized by Iranian forces, and Linerlytica estimates roughly 170 containerships totalling about 450,000 TEU — 1.4% of the global fleet — remain inside or adjacent to the strait under exit restrictions. Windward analytics show approximately 3,200 vessels still positioned west of Hormuz awaiting clarity.

The commercial picture has bifurcated. COSCO completed a second Hormuz exit attempt after an initial abort, and Lloyd's List reports the carrier transited boxships once Iran widened its approved-nation list. Maersk moved a vessel through the strait on May 5 under U.S. military protection, while six India-flagged ships completed the first coordinated bilateral cluster transit under Tehran's operational assurances. These selective passages stand in sharp contrast to the broader picture: dark-vessel activity surged nearly 600% between April 19 and May 3, GPS jamming impacted around 470 vessels in 24 hours near Fujairah and Khor Fakkan, and IRGC fast-craft swarm formations have been observed escorting commercial traffic.

This administrative layer is hardening into policy. On May 16 the Chair of Iran's Parliament National Security and Foreign Policy Committee, Ebrahim Azizi, confirmed Tehran will 'unveil soon' the full details of a new mechanism to regulate maritime traffic through Hormuz, including fees collected by a Persian Gulf Strait Authority for 'specialized services'. The May 6 strike on a French container ship and subsequent U.S. responses underscore how fragile the diplomatic framework remains.

On the rates side, the Hormuz pressure plus tightening Asia–Europe capacity is driving an early peak season. Freightos data shows Asia–North Europe spot rates climbed to about $2,900/FEU, matching the March war-time high, while Asia–Mediterranean spot rates surged 20% to nearly $4,400/FEU. CMA CGM, Hapag-Lloyd and MSC implemented new FAK rates effective May 15 ranging from $3,500 to $4,500/FEU on Asia–North Europe and $4,500 to $4,600/FEU on Asia–Mediterranean. Cape of Good Hope rerouting continues to absorb roughly 2.5M TEU of global capacity. Equipment imbalances are now the lingering structural problem for shippers: empty repositioning back to Asian hubs from the Gulf remains effectively impossible, tightening export box availability in North America and parts of Europe. Saudi Aramco's CEO warned that if Hormuz disruption persists, the oil market will not normalize until 2027.

After nearly three months of effective closure, the Strait of Hormuz crisis is showing the first credible signs of de-escalation. On May 23, President Trump declared a peace deal reopening the Strait 'largely negotiated', with Iran's foreign ministry confirming a memorandum of understanding as the first phase, followed by broader talks within 30-60 days. Iran's IRGC Navy has begun selectively clearing vessels — 33 ships, including oil tankers, transited in the past 24 hours, though approximately 240 vessels remain queuing for permission.

For container shipping, the unwinding will be slow. Of the 53 container vessels originally trapped inside the Persian Gulf when carriers suspended Gulf service in late February, only 9 have successfully exited — 81% remain locked in. Operation Project Freedom, Trump's May 4 initiative to escort merchant ships out of the Gulf, was paused after just 48 hours with only two vessels successfully guided through. The CMA CGM San Antonio was struck by a cruise missile on May 5, injuring eight crew, underlining that the security environment remains fragile.

The rate picture has stabilized faster than expected. Far East to Mediterranean spot rates sit at $3,451/FEU — just 4% above pre-crisis levels — while Far East to North Europe is at $2,531/FEU. Carrier workarounds (Cape of Good Hope rerouting, emergency trucking corridors through Saudi Arabia/Iraq/Jordan/UAE, redesigned service networks) are functioning well enough that underlying overcapacity is reasserting itself.

Equipment imbalances remain the structural risk: roughly 3 million TEU of global capacity is tied up in port delays, Jebel Ali congestion continues to grow, and empty container repositioning to Gulf origins is still impossible. DHL forecasts full normalization will take 4-6 months even after a political settlement — meaning the equipment ripple effect will run well into Q4 2026.

Day 84 of the Hormuz disruption marks a structural shift: Iran has moved from de-facto control to de-jure tolling. On May 18, Tehran's Supreme National Security Council activated the Persian Gulf Strait Authority (PGSA) — formalizing a permit-and-fee regime that has been operating informally since March. The PGSA requires vessel operators to submit full documentation (ownership, P&I cover, crew lists, cargo manifests, intended routing) via a designated email channel; transit is approved only after payment, reportedly up to $2M per vessel and settled in Chinese yuan.

The transit numbers tell two stories. IRGC state media reported 26 ships (May 20) and 31 ships (May 21) cleared under its coordination — including container ships. IMF PortWatch data captured only 2 actual transits on May 21 against a 95/day pre-crisis baseline. The methodology gap matters: container lines are not yet returning to the strait at scale.

For container shipping the operational picture has not improved. Kpler's two-month review confirms 81% of the 53 boxships initially trapped inside the Persian Gulf are still there — only 9 have exited, while 2 MSC vessels were seized by Iranian forces. Roughly 170 containerships and 450,000 TEU of capacity (~1.4% of the global fleet) remain commercially marooned.

Rate signals are mixed but firm-to-rising on the lanes most exposed to Hormuz-driven fuel costs. Asia-North Europe spot rates climbed 10% week-on-week to $2,850/FEU per Freightos. Maersk's Vincent Clerc has publicly quantified the carrier's exposure at $500M/month in additional bunker costs, and confirmed those costs are being passed through. Gulf-origin cargo carries emergency surcharges of $1,500-$4,000/TEU where bookings are accepted at all.

For forwarders and shippers, the planning posture remains unchanged: assume no commercial liner service through Hormuz, route Gulf cargo via Jeddah/UAE land-bridges or alternative Indian Ocean gateways, build the new fuel surcharges into Q3 contracts, and watch the PGSA fee structure — if Iran publishes a formal tariff and carriers begin paying it, that is the trigger to re-evaluate Gulf service restoration.

Two months into the Strait of Hormuz crisis, the container market is no longer waiting for a single resolution event — it is adapting to a structurally controlled chokepoint. The US Navy's 'Project Freedom' escort operation launched May 4 with the high-profile transit of Maersk's US-flagged Alliance Fairfax through an 'enhanced security corridor' inside Omani waters. Within 36 hours President Trump paused the operation, citing diplomatic talks with Tehran.

The pause was reinforced the next day when CMA CGM's Malta-flagged San Antonio was struck by an Iranian projectile during a night transit near Oman, injuring eight crew — the 32nd shipping incident since hostilities began. Maersk has kept its Hormuz suspension in place, citing 'wavering confidence' in the ceasefire even as Pentagon chief Hegseth says the truce holds.

Kpler data from May 7 shows 42 of the original 53 trapped container vessels remain inside the Gulf, with only nine successful exits, two MSC vessels seized by Iranian authorities, and one damaged by debris. The commercial response is now a structural shift: MSC launched a new bypass service on May 10 linking Baltic and North European ports through Suez to Aqaba, King Abdullah Port and Jeddah, with an onward land bridge across Saudi Arabia to the UAE.

Freight rates reflect the capacity squeeze: Asia–North Europe FBX11 rose 11% to $2,707/FEU and Asia–Mediterranean FBX13 jumped 15% to $3,850/FEU in early May, while transpacific Asia–USWC ticked up 8% to $2,127/FEU. Cape of Good Hope rerouting continues to absorb roughly 2.5 million TEU of global capacity and adds 7–14 days to Asia–Europe transit. Hapag-Lloyd's $1,500/TEU war-risk surcharge remains in force.

The US naval blockade of Iranian ports enters its 35th day with no breakthrough in sight. Trump on May 13 declared the ceasefire on 'massive life support' and dismissed Iran's latest counter-proposal as 'a piece of garbage,' while Iran's First Vice President Mohammad Reza Aref doubled down: 'Our right to the Strait of Hormuz is established, and the matter is closed.' The IRGC Navy has now formally redefined Hormuz as a 'vast operational area' stretching from Jask to Siri Island.

For container shipping, the most important development is structural, not tactical: the world's top carriers are no longer treating the closure as a temporary detour. Maersk's Middle East Operational Update 30 (May 12) confirms that key services remain rerouted around the Cape of Good Hope and consolidated through Salalah, with strict empty-return windows. MSC has launched a new Europe-Red Sea-Middle East service via Aqaba, King Abdullah and Jeddah, while Hapag-Lloyd is rolling out feeder networks that fully bypass direct Arabian Gulf calls.

The rate picture is the most counter-intuitive signal of the week. Asia-N. Europe spot has slipped back to $2,707/FEU (only $100 above late-February pre-war levels) and Asia-Med sits at $3,850/FEU — well below the early-April spike. The reason: Cape capacity absorption is now priced in, and pulled-forward bookings are stabilising. But carriers and forwarders are warning of an unusually early peak season as shippers front-load Q3 volume.

On May 16, Kpler tracked just 16 vessels through the strait (6 inbound, 10 outbound) — overwhelmingly flags of convenience (Bolivia, Comoros, Iran, Antigua); mainstream box lines remain absent. Equipment imbalances continue to deepen, with empty repositioning to Gulf origins effectively impossible and congestion at Jeddah, Khorfakkan, Sohar, Fujairah and Salalah accumulating demurrage from day 5-7 of free time.

Eleven weeks into the Strait of Hormuz crisis, the picture has split in two. On the water, the situation remains acutely critical: 53 containerships belonging to the world's top liners are still trapped inside the Persian Gulf, and Kpler container data shows 81% of vessels caught when the strait effectively closed in late February are still waiting. Escape attempts have produced a clear hierarchy — COSCO leads with a 40% extraction rate, MSC has managed 29% (offset by two of its vessels being seized by Iran), and most other operators have failed to move a single ship out.

MSC has roughly 109,000 TEU of capacity marooned in the Gulf, Maersk around 70,000 TEU. The May 6 strike on a French-flagged container ship near the strait, followed days later by Iranian seizure of a tanker and US 'disabling' actions against two vessels, confirmed that even partial transits remain genuinely dangerous. President Trump's 'Project Freedom' US Navy escort initiative has been paused while Washington and Tehran resume direct negotiations.

Iran has unilaterally established a 'Persian Gulf Strait Authority' under the IRGC, requiring vessels to request transit permission; the UN maritime chief and US State Department have both rejected the framework as inconsistent with UNCLOS.

On the rate side, the shock has largely been absorbed. Xeneta's May 14 update shows Far East–Mediterranean spot rates now only 4% above pre-crisis levels. The structural capacity glut — heavily oversupplied newbuilds against demand that has not recovered — is offsetting what would otherwise have been a far sharper price spike. Carriers have reorganized around the disruption: Maersk is rerouting most Middle East services around the Cape of Good Hope and transhipping via Salalah Port, Hapag-Lloyd has introduced a revised feeder network that avoids direct Arabian Gulf calls, and MSC has launched a new Europe–Red Sea–Middle East service. Equipment imbalances continue to deepen — empty repositioning to Gulf origins remains nearly impossible — and even if a diplomatic settlement is reached, industry analysts expect months to clear the backlog.

Thirty days into the US naval blockade of Iranian ports and the Strait of Hormuz, the container shipping industry has moved decisively from emergency response to permanent network redesign. President Trump paused the 'Project Freedom' escort operation on May 5 to support Pakistan-mediated talks with Tehran, but the underlying naval blockade remains in force and Iran responded by formalising the 'Persian Gulf Strait Authority' — a permanent body to regulate, charge and clear every vessel transit.

The day before the pause, the CMA CGM 'San Antonio' was struck by a projectile during a night transit, with injured crew evacuated; it is the second CMA CGM incident in the strait in a month. For container shipping, the strategic question has shifted from 'when does Hormuz reopen' to 'how do we permanently bypass it'.

Maersk continues to suspend most Gulf crossings and is rerouting key Middle East services via the Cape of Good Hope, leaning on Salalah as a transhipment hub. Hapag-Lloyd has rolled out revised feed-based networks that avoid direct Arabian Gulf calls, while MSC launched a fresh Europe–Red Sea–Middle East service built around Aqaba, King Abdullah and Jeddah.

After three consecutive weekly declines, container spot rates snapped back this week as carriers pushed a new wave of emergency fuel and peak-season surcharges tied to Hormuz risk and feeder rerouting. Maersk's Q1 2026 print — EBITDA of $1.8B and ocean volumes up 9.3% YoY — shows the majors can absorb the structural shock, but Goldman Sachs estimates the GCC is losing roughly $700M per day in unmoved oil and gas exports. Equipment imbalances continue to deteriorate: empty container repositioning to Gulf origins is effectively impossible, backlogs at feeder hubs are deepening, and even a peace deal would leave weeks of suspended sailings and stranded boxes to unwind.

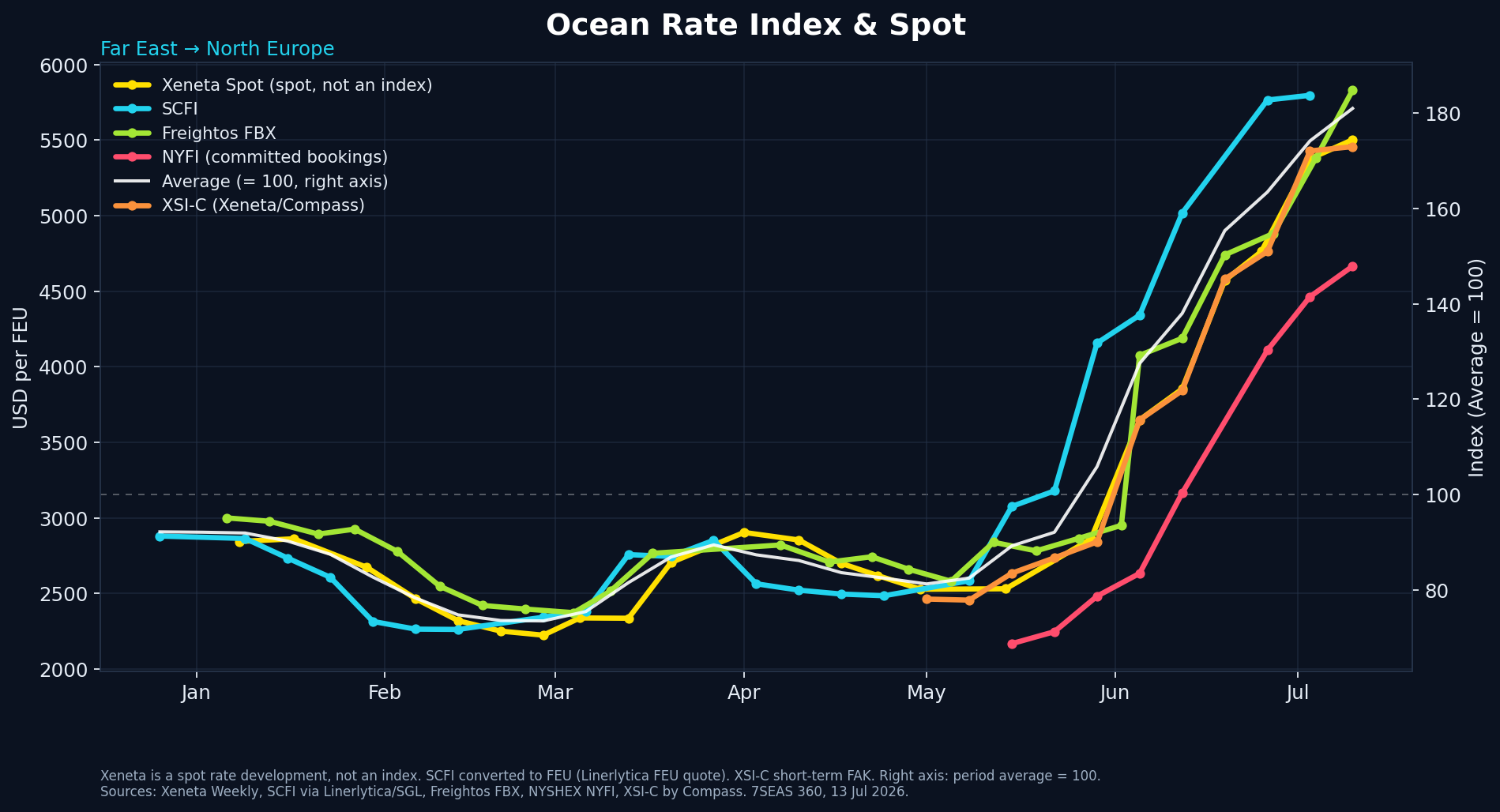

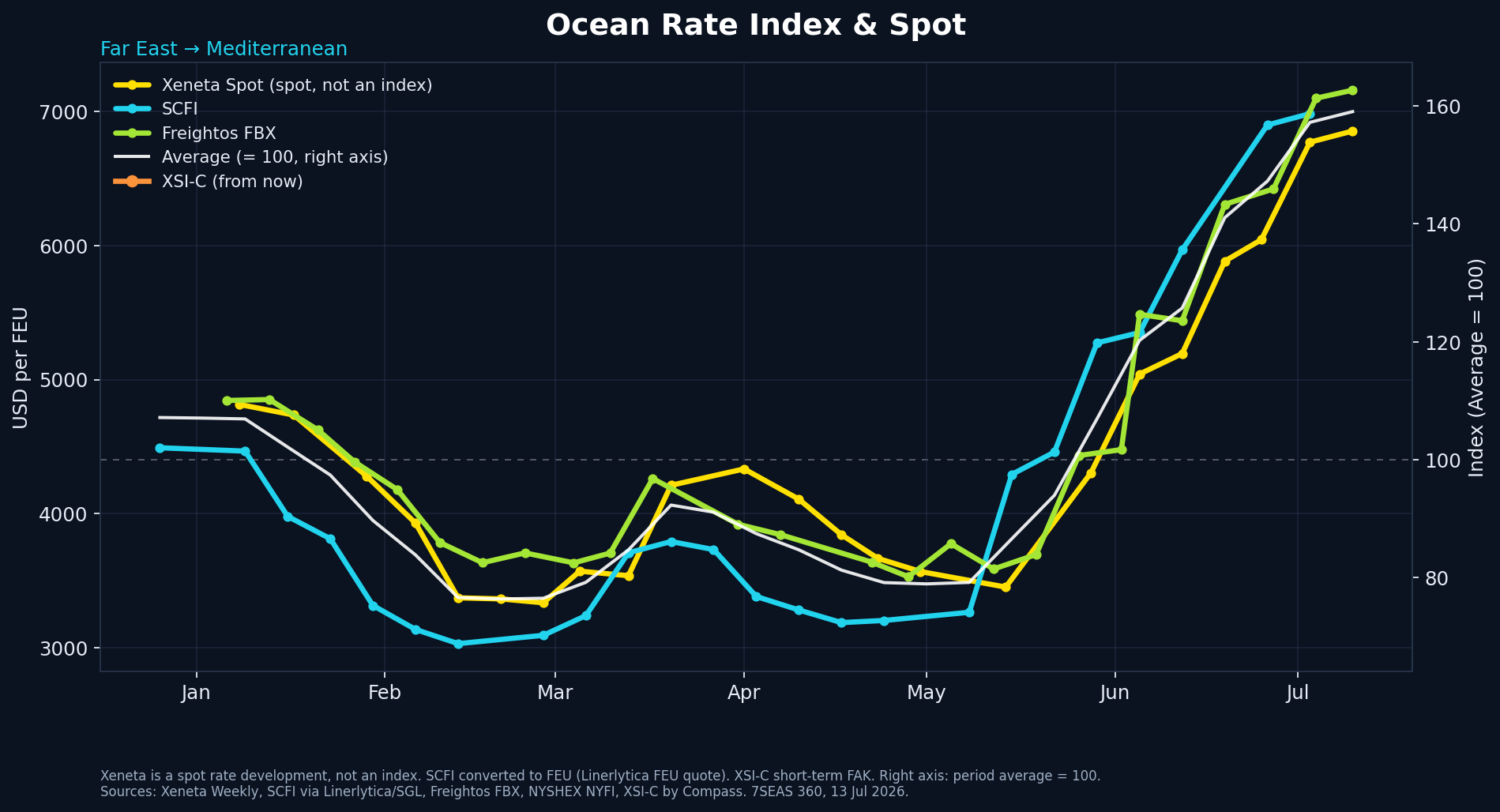

This week the container read on the Red Sea shifts from routing announcements to hard traffic data, and the two do not point the same way. On volume, the return is real. Lloyd's List puts Bab el-Mandeb at 1,338 vessel transits in June, the busiest month since December 2023 and 39 percent above a year earlier, with large containership transits up 215 percent across the first half of 2026. Suez Canal traffic has climbed about 26 percent over the same window to its highest level since January 2024. That is the clearest sign yet that the corridor is being used again rather than merely talked about, though every figure still sits well under pre-crisis norms and the pickup only accelerated once renewed Hormuz disruption made the Red Sea look like the lesser risk. The carrier decisions underneath the data are the ones already on record, now showing up in the transit counts: the Gemini AE15 service testing Suez since 6 July after the Majestic Maersk cleared Bab el-Mandeb, and Maersk's solo MECL service moving back to the trans-Suez route, both kept expressly conditional on security holding. Against that firming traffic, the price signal is going the other way. Linerlytica reports that carriers have begun rolling back their North Europe rates, with first-half July spot failing to breach $6,000 per 40ft and the Gemini partners undercutting at around $4,800 against rivals asking $6,000 to $6,500. A round of general rate increases and peak-season surcharges scheduled for 15 July is the near-term test of how much real peak demand remains. For shippers the practical read is that capacity is genuinely trickling back to the Red Sea and the traffic data now backs it, while rates still rest on peak-season demand rather than on the canal, so a soft mid-July GRI would be a demand signal, not a Red Sea signal. Keep planning against both lanes, and watch whether the transit recovery survives the next security scare rather than pricing in a settled reopening.

The container read on the Red Sea this week is about price, not a single incident. From 15 July 2026 the Suez Canal Authority raises its transit surcharge on containerships to 12 percent, applied to any vessel that begins transit on or after that date. Containers get off lighter than most segments in the same revision: dry bulk carriers jump from 10 to 22 percent, general cargo and ro-ro rise to 26 percent, and laden crude tankers face 37 percent on top of the base toll, with passenger ships the only class left untouched. The timing matters because the increase lands while carriers are still deciding whether to bring services back off the Cape of Good Hope, so it lifts the toll cost of every Suez routing they might restore. What makes the move awkward to read is that it comes from the same authority that has spent months trying to lure carriers back. Cairo has offered incentives, including a 15 percent discount for large boxships of 130,000 GT and above, and Chairman Ossama Rabiee has personally visited ships to demonstrate readiness for full-size operations. A broad surcharge and a targeted discount for the largest vessels point in opposite directions, and the SCA itself says the fees rest on its assessment of market conditions and may be amended or cancelled. For shippers the underlying posture has not changed. Most Asia to Europe capacity still runs via the Cape, Xeneta's Peter Sand continues to judge a large-scale container return to the Red Sea unlikely in 2026 on security grounds, and the single live test remains the Gemini AE15 string that Maersk and Hapag-Lloyd started routing through Suez on 6 July. Rates stay elevated on peak-season demand rather than the canal, with Freightos FBX Asia to North Europe last assessed near $4,900 per FEU in early July. Treat the 15 July surcharge as a cost input to fold into any Suez-versus-Cape comparison, and keep watching whether the AE15 test survives the next security scare rather than pricing in a lane-wide reopening.

The container story on the Red Sea has moved from watching an attack to watching a routing decision. On 6 July, Maersk and Hapag-Lloyd told customers that their AE15 service, which links Asia with the Mediterranean and Europe, will shift from the Cape of Good Hope back to the trans-Suez route, beginning with the Triple-E boxship Majestic Maersk. This is the first expansion of the Gemini Cooperation's Suez network since the two carriers were forced to pull their ME11 and MECL services off the Red Sea in March, after an earlier February return proved short-lived. The AE15, calling at Qingdao, Kwangyang, Ningbo, Tanjung Pelepas, Port Said, Damietta, Colombo and Singapore, will once again use the fastest Asia to Europe corridor and shorten transit against the long route around southern Africa. The carriers were careful to bound the decision. They said it follows thorough assessments of the security situation, that they have no current plan to bring more Gemini services back to Suez or to rebuild their broader east-west network to pre-crisis routing, and that they are ready to send the AE15 back around the Cape if the picture worsens. That caution is not boilerplate. It sits directly against the 5 July attack on a cargo ship about 30 nautical miles southwest of Al Hudaydah, the first reported strike on a commercial vessel in the lane since the October 2025 Gaza ceasefire, which no group has claimed and which is still under investigation. Gemini's own history frames the risk: its February ME11 return was reversed within weeks. For shippers the practical read is unchanged in substance but sharper in signal. Most capacity still runs via the Cape, one service is testing Suez again on a single Gemini string, and rates remain elevated on peak-season demand rather than the canal, with Freightos FBX Asia to North Europe last assessed near $4,900 per FEU in early July. Treat AE15 as a service-specific exception to monitor, not a lane-wide reopening, and watch whether it holds through the next security scare rather than pricing in a permanent Suez return.

The Red Sea produced its first reported attack on a commercial ship since the October 2025 Gaza ceasefire. On 5 July, about 30 nautical miles southwest of Al Hudaydah in Yemen, a cargo ship reported that a skiff approached and opened fire. The ship's armed guards returned fire, and the skiff pulled back to a larger vessel roughly two nautical miles away that had its AIS transponder switched off. The ship and its crew were reported safe, and UKMTO advised vessels to transit with caution. No group has claimed the attack and the identity of the attackers is not confirmed, so this is a warning signal rather than a confirmed return of the Houthi campaign. It still matters for container shipping because it breaks the calm that has held on the lane since the ceasefire and tests the assumption behind the slow, service-specific return to Suez. The context is a standing threat: on 8 June the Houthis declared a ban on Israeli-linked shipping in the Red Sea and kept any broader action tied to Gaza and the ongoing Iran conflict. For now the routing picture is unchanged. Most lines still send Asia to Europe cargo around the Cape of Good Hope, adding 10 to 14 days, and no major carrier has announced a change to its Red Sea plans in response to this incident. Rates stay high on peak-season demand rather than the canal, with Freightos FBX Asia to North Europe last assessed near $4,900 per FEU on 2 July. The practical message for shippers holds: plan around Cape transit times and a firm rate environment, treat any Suez routing as a per-service exception, and watch whether this attack is a one-off or the start of a pattern before reading it as a shift in the lane.

The Suez corridor is recovering by inches. About 35 cargo vessels transited the canal in the week to 28 June, and Maersk has now run three westbound sailings on its Middle East Container Line through the Bab-el-Mandeb Strait since 13 June. That is movement, but it is not a market shift. Most lines still route Asia to Europe cargo around the Cape of Good Hope, which adds 10 to 14 days, and the carriers testing the canal frame it as service-specific rather than a broad reopening. The dominant force on rates right now is peak season, not routing. Freightos FBX shows Asia to North Europe at $4,900 per FEU, up 70 percent since mid-May, and Asia to Mediterranean at $6,500 per FEU, up 85 percent, both now above their 2025 peak-season highs. An early frontloading rush, port congestion at major hubs, and July general rate increases are all pushing prices up. The security picture stays the deciding factor for the lane. The Houthis have not hit a commercial ship since the October 2025 Gaza ceasefire, yet they keep their threat tied to Gaza and the wider Iran conflict, which is enough to hold most carriers off the Red Sea. That caution was reinforced over the weekend, when Iranian strikes near the Strait of Hormuz hit several vessels, including a container ship that was not in the designated Iranian transit lane, and the IMO paused its phased Hormuz evacuation in response. For shippers the practical message holds: plan around Cape transit times and a rising rate environment, treat any Suez routing as a per-service exception, and watch the Iran track closely because it now shapes container risk on both chokepoints.

The Suez corridor is reopening in slow motion. Maersk, among the more risk-averse carriers, has now run its first container voyages back through the canal since early March, a notable signal because it puts the line ahead of its Gemini partner Hapag-Lloyd, which is holding its long-haul services on the Cape of Good Hope. Ocean Network Express remains cautious as well, with all of them stressing that the security picture, not commercial pressure, will set the pace of any wider return. Linerlytica reads the same data and expects only a gradual, selective recovery, with canal volumes approaching normal late in 2026 rather than now. Rates are firming in the meantime. Freightos FBX shows Asia to North Europe at $2,707 per FEU and Asia to Mediterranean at $3,850 per FEU, both up double digits, and carriers have already announced July increases of up to $2,000 per FEU. The geopolitical backdrop stays unsettled. The Houthis continue to designate Israeli-linked vessels as legitimate targets, and while a reported US-Iran interim deal could reopen the Strait of Hormuz within roughly a month, that easing has not yet pulled container traffic back into the Red Sea at scale. For shippers, the practical message is unchanged: plan around Cape transit times and elevated rates, and treat any Suez routing as service-specific rather than a market-wide shift.

The Red Sea return stayed frozen in the last week of June 2026 as the wider Gulf picture turned volatile again. After the US and Iran signed a memorandum on 16 to 17 June to reopen the Strait of Hormuz without tolls for at least 60 days, Iran's Revolutionary Guard declared the strait shut over 20 to 22 June, citing Israeli strikes in southern Lebanon and a breakdown in the ceasefire. US Central Command disputed the move, reporting 55 merchant transits on Saturday and describing safe passage as intact, while the US energy secretary said on 24 June that Washington had removed Iran's ability to close the waterway. The ship-tracking picture sat between the two claims: Windward recorded Hormuz transits dropping to 12 vessels on Sunday from 35 the day before, with five of eight inbound ships sailing dark, a pattern it likened to the late-blockade period rather than a functioning open strait. For container shipping the practical read is unchanged but reinforced. The main box loops transit Bab-el-Mandeb, not Hormuz, so the direct effect on container routing is limited, yet the renewed instability keeps war risk premiums elevated and pushes carriers to stay cautious on any Suez return. Maersk continues a measured, structural return on selected services, while CMA CGM keeps its Asia–Europe loops around the Cape of Good Hope. Suez container transits remain roughly 60% below the pre-crisis baseline and the Cape detour still adds about 10 to 14 days on Asia–Europe, so shippers continue to manage two parallel networks with different transit times and reliability. War risk underwriters are holding a wait-and-see line and premiums stay high. Asia–North Europe long-term rates near USD 2,010 per FEU have eased from the crisis peak but remain anchored to the longer routing most capacity still follows, and Freightos cautions that a real shift back toward Suez would first create congestion and upward spot pressure as patterns readjust. The MARAD advisory 2026-006 covering the Red Sea, Bab-el-Mandeb, Gulf of Aden, Arabian Sea and Somali Basin runs to 22 September 2026. A full, stable Suez return looks unlikely while the Hormuz and wider ceasefire picture stays this fragile.

The widely forecast return of container shipping to the Red Sea has lost momentum in June 2026. After early-year moves by Maersk and CMA CGM to test Suez routings, the two largest carriers have now diverged. Maersk is maintaining a measured, structural return on selected Asia–Mediterranean and Asia–Europe services, while CMA CGM has reversed its decision and sent the affected loops back around the Cape of Good Hope. The trigger is a fresh round of Houthi attacks: since 5 June the group has targeted at least six vessels, selecting ships by their operators' links to Israeli ports rather than by flag. Confirmed damage to the bulk carrier Verbena in the Gulf of Aden on 13 June underlined that the threat remains live across the wider Bab-el-Mandeb and Gulf of Aden corridor. The MARAD advisory 2026-006 covering the Red Sea, Bab-el-Mandeb, Gulf of Aden, Arabian Sea and Somali Basin now runs to 22 September 2026. For container shippers the practical effect is a fractured network. Suez transits stay near 60% below the pre-crisis baseline, the Cape detour still adds roughly 10 to 14 days on Asia–Europe, and the carrier split forces shippers to manage two routing patterns with different reliability and cost profiles at once. Asia–North Europe long-term rates near USD 2,010 per FEU have eased from the crisis peak but remain anchored to the longer routing that the bulk of capacity still follows. The geopolitical backdrop, including wider regional tension around the Strait of Hormuz, keeps risk premiums and insurance terms elevated and makes a full, stable Suez return unlikely in the near term.

The sharpest signal for shippers this week sits in the rate sheet, not the threat board. Drewry's World Container Index has climbed to $3,969 per 40ft container, a 12% weekly gain that marks an 18-month high, and the Asia-Europe lane is leading it: Shanghai-Rotterdam jumped 15% to $4,342 and Shanghai-Genoa rose 12% to $5,756. The driver is the same structural squeeze that has defined the crisis. With most eastbound capacity still steaming around the Cape of Good Hope to avoid Bab el-Mandeb, a large share of the global fleet stays tied up in extra sea miles, and that scarcity is now meeting an early peak season as cargo is pulled forward ahead of the 1 July bunker adjustment and expected US tariff changes. Maersk's revised peak season surcharge of $1,500 per 40ft box from Far East Asia to North Europe and the Mediterranean, effective 7 July, points to further upward pressure rather than relief. The geopolitical shift this week landed on the Gulf side. A US-Iran interim agreement signed on 15 June reopened the Strait of Hormuz with 60 days of toll-free commercial transit, and Kpler tracked supertankers resuming passage within days, easing the perceived risk that had hung over the strait and lifting overall shipping sentiment. For the container market through Bab el-Mandeb, however, that deal changes little. The Houthi ban on Israel-linked navigation and the first kinetic strikes since September 2025, two vessels hit in the Gulf of Aden on 8-9 June, remain the binding constraint on the southern route, and Maersk is holding its Gulf restrictions and emergency surcharges in place despite the Hormuz reopening. Suez throughput stays roughly 60% below pre-crisis levels. For forwarders and shippers the message is consistent: a calmer Hormuz does not reopen the Red Sea, the Cape premium stays embedded in pricing, and elevated, volatile rates should be planned for into the second half of 2026.

Two weeks of escalation have left the Red Sea corridor in a familiar but tense position: security risk is back on the table, yet the sharpest near-term signal for shippers is in the rate sheet. Drewry's World Container Index has climbed to $3,969/feu, a 12% weekly jump that puts spot pricing within reach of $4,000 and well above pre-crisis norms. The driver is not a fresh attack but structure plus timing. With most Asia-Europe services still steaming around the Cape of Good Hope to avoid Bab el-Mandeb, a large slice of global fleet capacity stays tied up in extra sea miles, and that scarcity has met an early peak season as cargo is pulled forward ahead of the 1 July bunker adjustment, anticipated US tariff moves and World Cup volumes. The security picture explains why the detour persists. A week after the Houthis declared a complete ban on Israeli navigation and struck two commercial vessels in the Gulf of Aden, their first kinetic enforcement since September 2025, the targeting logic has widened to any operator that has called at Israeli ports. That keeps a broad pool of tonnage exposed and the wider Iran-Israel truce, reached in April, fragile after renewed missile exchanges from 7 June. Carriers are responding in different directions, with Maersk pulling services back to the Cape while CMA CGM presses ahead with a Q2 Suez return, so there is no single industry read on the strait. For forwarders and shippers the message is consistent: expect the Red Sea premium to stay embedded in pricing, and plan for elevated, volatile rates into the second half of 2026.

After eight months of relative calm, the Red Sea corridor has slipped back into crisis. On 8 June, Houthi military spokesman Yahya Saree announced a complete ban on Israeli maritime navigation in the Red Sea, and within hours the threat turned kinetic: two commercial vessels were struck in the Gulf of Aden on 8-9 June, the first attacks on merchant shipping since the Minervagracht in late September 2025. The targeting logic has hardened in a way that matters to every forwarder and carrier. Neither ship was Israeli-flagged; both were hit because their operators had recently called at Israeli ports, meaning exposure now follows corporate port-call history rather than flag state alone. For container lines that had cautiously begun testing Suez routings, the message landed quickly. Maersk has again pulled some services back around the Cape of Good Hope, citing constraints in the operating environment after talking to its security partners, while CMA CGM holds to its more aggressive Q2 return and Hapag-Lloyd waits on the sidelines. The result is a fragmented industry with no shared read on Bab el-Mandeb. For now, the broader market shock is muted because traffic through the strait is already thin, around half its pre-crisis level, and current rate strength is driven mainly by an early peak season rather than the renewed attacks. The strategic picture, though, has clearly deteriorated: the resumption of strikes and the reversal of carrier returns suggest the Cape detour, and the capacity it absorbs, will persist well into the second half of 2026.

The Red Sea corridor has slipped back into full crisis mode. The 10 June small-boat attack near Bab el-Mandeb, in which embarked security teams exchanged fire with six armed assailants before the craft broke away, is the clearest signal yet that the Houthi threat to merchant shipping is active again, not rhetorical. With the group now openly aligned with Tehran in the wider conflict and a declared ban on 'enemy navigation', insurers and operators are treating the southern Red Sea as a no-go area for most container tonnage. For shippers, the practical consequence is that the Cape of Good Hope routing remains the default for Asia-Europe and Asia-Med services, adding 10 to 14 days per voyage and absorbing significant capacity. That capacity squeeze, combined with importers front-loading peak-season cargo, is driving spot rates sharply higher: the Shanghai-Rotterdam benchmark jumped 25% in a week to USD 3,579 per FEU, and carriers are layering on peak season surcharges of up to USD 1,000 per FEU. The simultaneous closure of the Strait of Hormuz compounds the disruption, cutting Gulf liner services off from mainline networks and forcing cargo onto feeder and overland alternatives. Industry consensus has shifted: a meaningful container return to the Suez route in 2026 is now off the table, and forwarders should plan networks, transit times and budgets around the Cape routing well into 2027.

The cautious return of container shipping to the Red Sea has stalled. On 8 June the Houthis announced a partial naval blockade amounting to a 'complete ban' on Israeli-linked vessels through the Red Sea and Bab-el-Mandeb, effective immediately, after Israel resumed strikes on Iran. A Houthi source told Reuters the ban is 'a first step' and that the movement could move to stop any ship bound for Israel if escalation continues. For box carriers, the timing erases the recovery narrative that had built up since late 2025, when CMA CGM ran ultra-large vessels back through Suez and Maersk completed its first transit in two years under a Suez Canal Authority partnership. That tentative reopening had already cracked: following the 28 February resumption of Houthi attacks, Maersk diverted selected ME11 and MECL sailings back around the Cape of Good Hope, and CMA CGM reverted its FAL services to the Cape, citing the fragile security environment. With this latest declaration, the default for the major networks stays Cape routing, keeping roughly 1.75 million TEU, some 5-6% of the global fleet, tied up on the long way round and leaving Suez container throughput far below pre-crisis levels. The practical read for shippers and forwarders: do not plan on a Suez switch this quarter. Asia-North Europe spot rates remain elevated at 25-40% above a no-crisis baseline, transit times stay stretched by the Cape detour, and any large-scale capacity release that a real return would unlock is again pushed out. The wider Israel-Iran exchange that triggered the announcement keeps Red Sea risk hostage to a conflict the shipping market does not control.